The month-end close is done. The numbers tie out, the balances agree, the trial balance sits neatly, and everyone signs off. The financial statement looks clean enough that even the strictest auditor wouldn't object at first glance. Then three months pass.

A customer calls: "We paid that invoice back in March." You pull the bank statement — they're right. The payment was made, the money genuinely landed in your account. So why did your ledger still show that invoice as open? Why was it in your collections list, in your aging report, inside your cash-flow forecast?

Your ledger wasn't wrong. It was incomplete. And that difference — the narrow gap between what is *wrong* and what is *incomplete* — is the most expensive, most invisible number on most companies' balance sheets. We call it the invisible balance sheet.

This article is about why that gap exists, why it stays invisible on its own, and what surfaces when you finally make it visible. It's written for the CFO, the controller, and the accountant — for everyone who signs "balanced" at close but privately wonders "did we, though?"

A record captures an event; reconciliation reveals a relationship

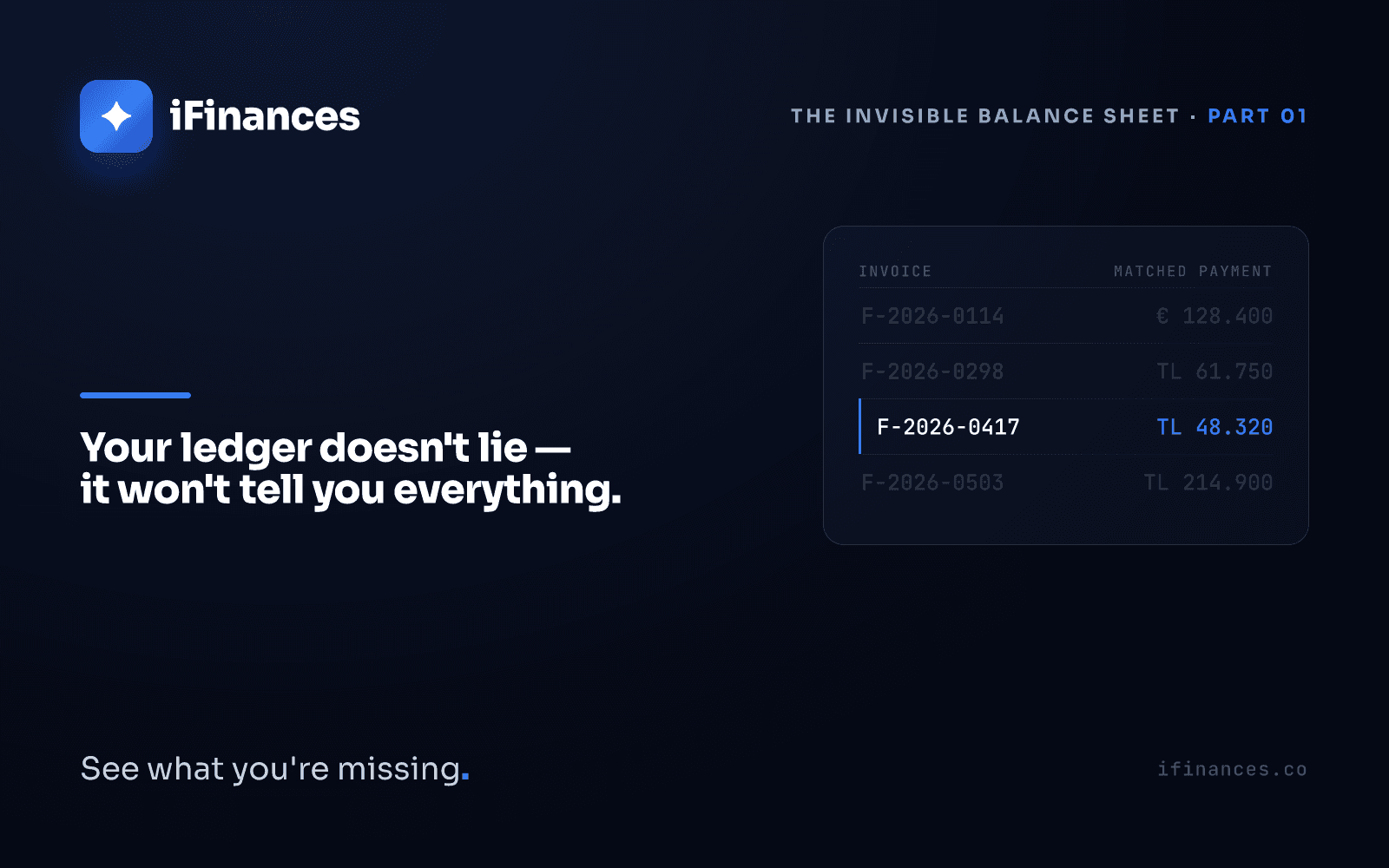

An accounting entry faithfully writes down what happened: an invoice was issued, money came in. Two lines, both correct. But the link between those two lines — which payment closed which invoice — is written nowhere automatically. The record captures the event; it doesn't capture the relationship.

Until that link is established, a payment is only "incoming money," and an invoice is only an "open receivable." That the two are in fact the same transaction — two ends of the same commercial relationship — only becomes clear once someone matches them. Reconciliation — the line-by-line verification of whether two parties (you and your customer, or your ledger and your bank statement) meet on the same numbers — is precisely the work of building that link. Keeping records is accounting; establishing the relationship is reconciliation.

A record captures an event; reconciliation reveals a relationship. The layer most companies can't see isn't the layer of records — it's the layer of relationships *between* records.

We explored why this distinction still gets trapped inside Excel, and why the spreadsheet breaks past a certain point, in our earlier piece on moving from Excel to financial intelligence. The core idea is the same here: the spreadsheet holds the record well; it can't hold the relationship at scale.

Why does the invisible balance sheet stay invisible?

The first explanation that comes to mind is bad intent or carelessness. It's almost never that. The cause is far more ordinary and far harder: scale.

Picture a single customer's single invoice. A payment arrives, closes the invoice, an entry is booked. Visibility is total. Now push that to the scale of a real company:

- A customer pays one invoice in three installments; which installment covers which remaining balance, and how much of it?

- Does a payment come off the oldest open invoice — this is FIFO, "first in, first out," the rule of closing invoices in sequence starting from the oldest open one — or off the reference in the transaction description?

- An invoice denominated in foreign currency is settled with a Turkish lira payment on a date when the exchange rate has moved; is the gap an error, or a normal FX difference between two dates?

- A bank statement description carries an order number but no company name. Whose money is this?

Each of these, on its own, can be resolved by a person in a single afternoon. But across tens of thousands of lines, multiple companies, two currencies, all at once — it moves beyond what one person and one Excel file can carry. Invisibility isn't negligence; it's the natural consequence of scale. A tired eye isn't defective; it simply wasn't designed to repeat the same five decisions flawlessly across tens of thousands of rows.

A single source is never enough

The second reason for invisibility is that the truth never lives in a single place. Your ledger tells one story. The counterparty's e-invoice tells another. The bank statement tells a third. All three are correct; all three are partial. You cannot know whether a receivable has truly closed by looking at your ledger alone — because the ledger doesn't see a payment that hasn't yet been matched.

This is why real reconciliation requires setting three sources side by side, not one. We detailed why and how in our piece on three-way reconciliation that cross-checks bank, e-invoice, and ledger. In short: if a number is identical across all three sources, you can trust it. If it appears in one source and not the other — that's exactly where the invisible balance sheet begins.

What surfaces when it becomes visible?

When you establish the links, when you bring that layer of relationships between records to the surface, four things typically appear. All four sit quietly beneath a balance sheet that looked "balanced" at close:

- Money collected but never applied to any invoice. These are receivables you thought were "open" that actually closed long ago. In accounting this is called unapplied cash: money collected but not posted to an invoice, sitting loose.

- Items that appear closed but were never actually paid. These are real receivables you forgot to collect, silently written off.

- Phantom balances that are neither payable nor receivable. Amounts that look "open" only because they didn't match — debts that don't actually exist.

- The true age of your receivables. The real picture of a 210-day risk you thought was 90 days old.

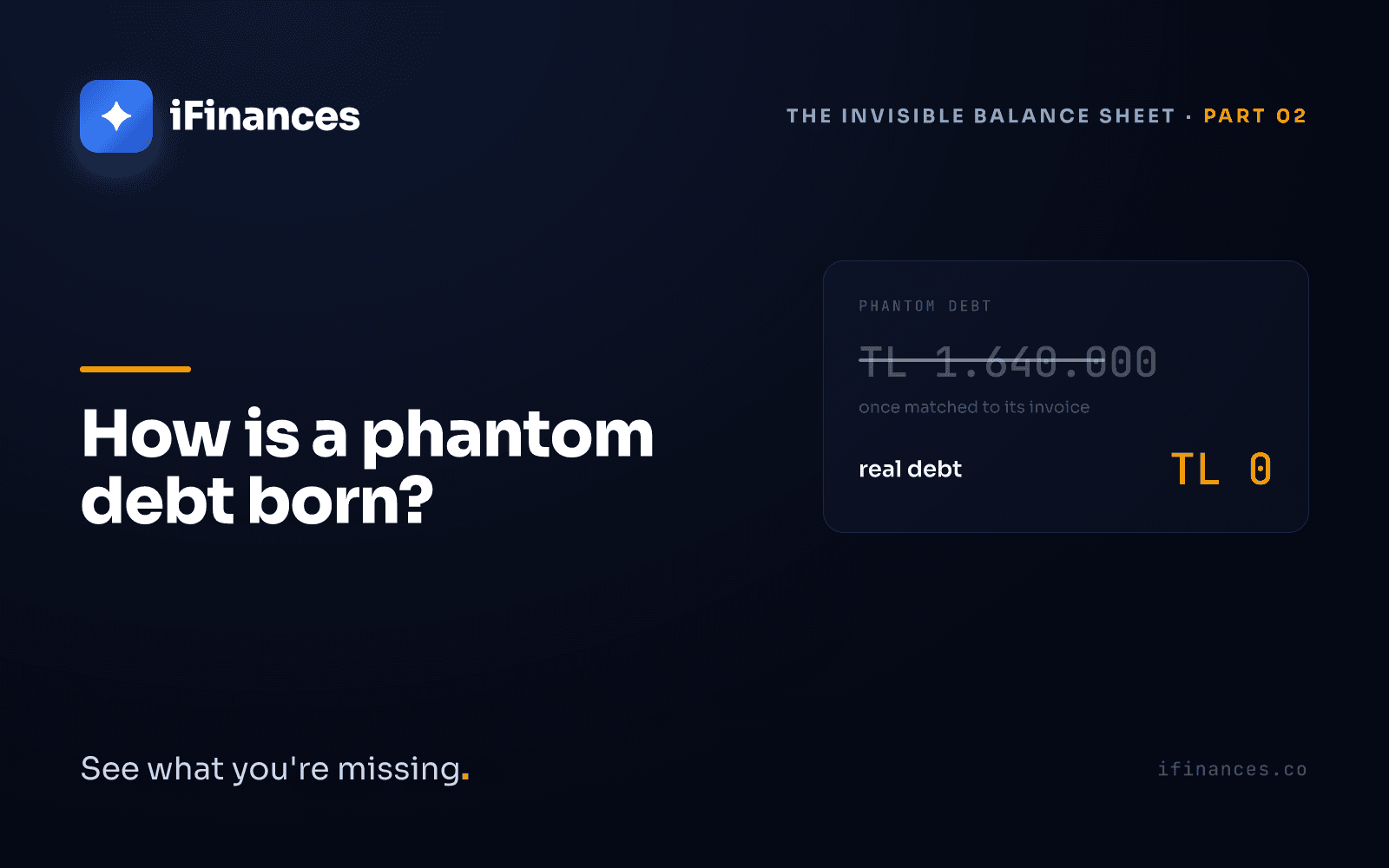

When the first and third of these mix together, the most expensive outcome arises. A paid-but-unmatched amount lives in your ledger for months as though it were a genuine debt. We call this phenomenon phantom debt, and we worked through the cost of chasing a customer for a debt that isn't there, one case at a time, in what phantom debt is, and why a paid invoice shows as open.

The balance sheet doesn't lie; it simply doesn't show this layer. The most expensive number isn't the wrong one — because a wrong number gets noticed and corrected one day. The most expensive number is the one no one can see; because you still make decisions on top of it.

The most expensive number isn't the wrong one

The error companies talk about most is the visible one: a mistyped amount, a flipped sign, a forgotten zero. It's uncomfortable but visible. One day it catches someone's eye, gets corrected, and closes.

The real cost lies in the number no one can see. Because:

- You can't collect a receivable you can't see — the money stays on the table.

- You can't manage a risk you can't see — if you think a 210-day receivable is 90 days old, you set aside no provision.

- You can't make sound decisions on a phantom debt you can't see — but you make them anyway, because that number looks real on your balance sheet.

This is not a failure of the accountant or the controller. On the contrary: when the tens of thousands of lines that *can* be matched systematically are handed to a machine, the human eye can finally focus on the minority that genuinely requires judgment — an ambiguous reference, an unusual pattern, a difference that needs explaining. iFinances doesn't replace the accountant; it surfaces and clears away the routine, leaving only the decision a human can make.

How iFinances makes this layer visible

We didn't build iFinances to rewrite your ledger. Our aim is to make visible what your ledger already says but can't show. Our product modules do this one job from three angles:

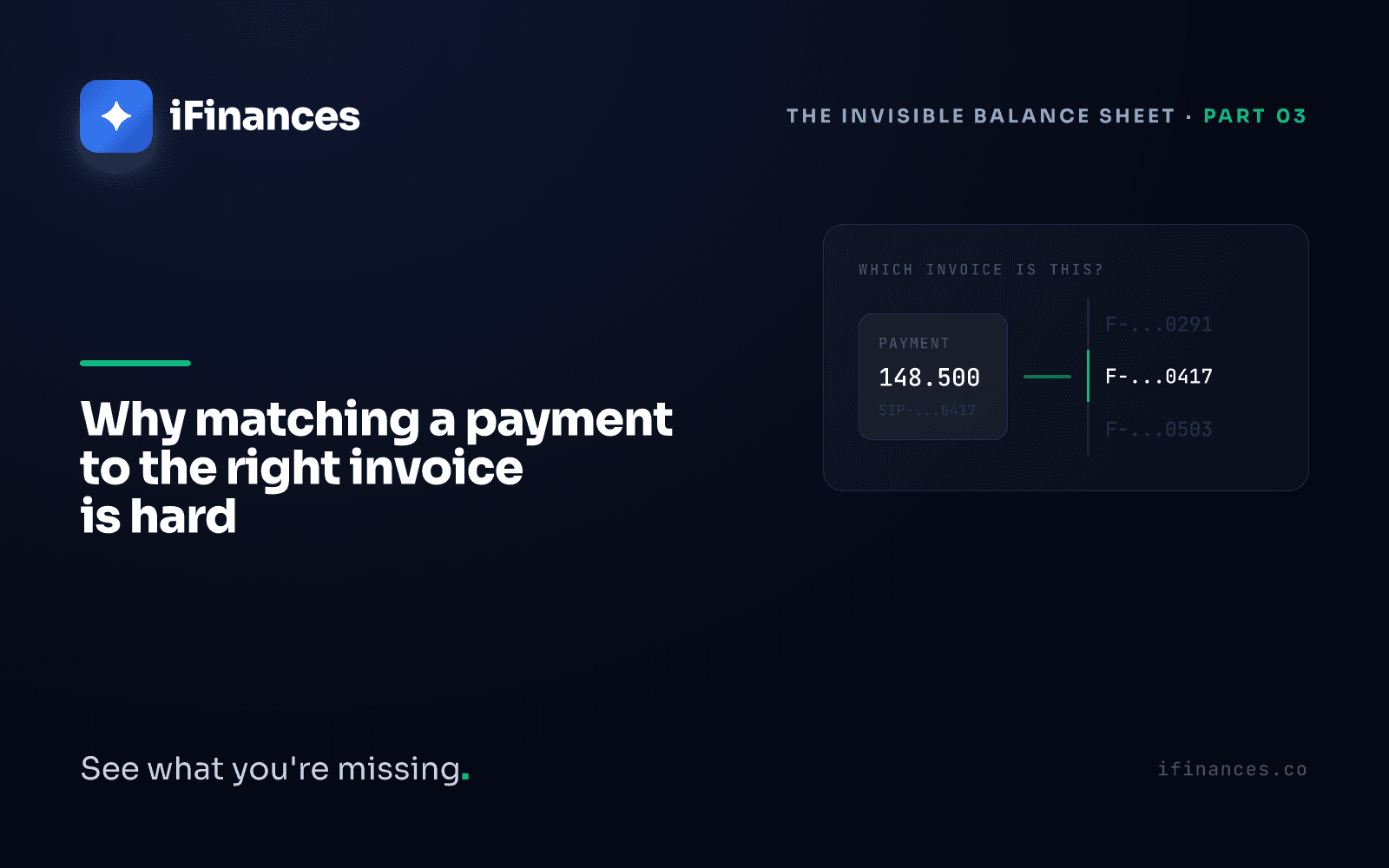

- [Matching](/en#eslestirme) links a payment to an invoice — working from company, amount, and date to mark the certain as certain and the ambiguous as ambiguous. On partial payments it applies FIFO discipline consistently; it reads the reference embedded in the description; it tracks third-party transfers beyond just the name.

- [Reconciliation](/en#mutabakat) sets your ledger, the e-invoice, and the bank statement side by side — showing line by line whether a number holds across all three sources. Why a number isn't merely "an Excel task" but is in fact a trust infrastructure is something we set out separately in reconciliation is not Excel, it's trust infrastructure.

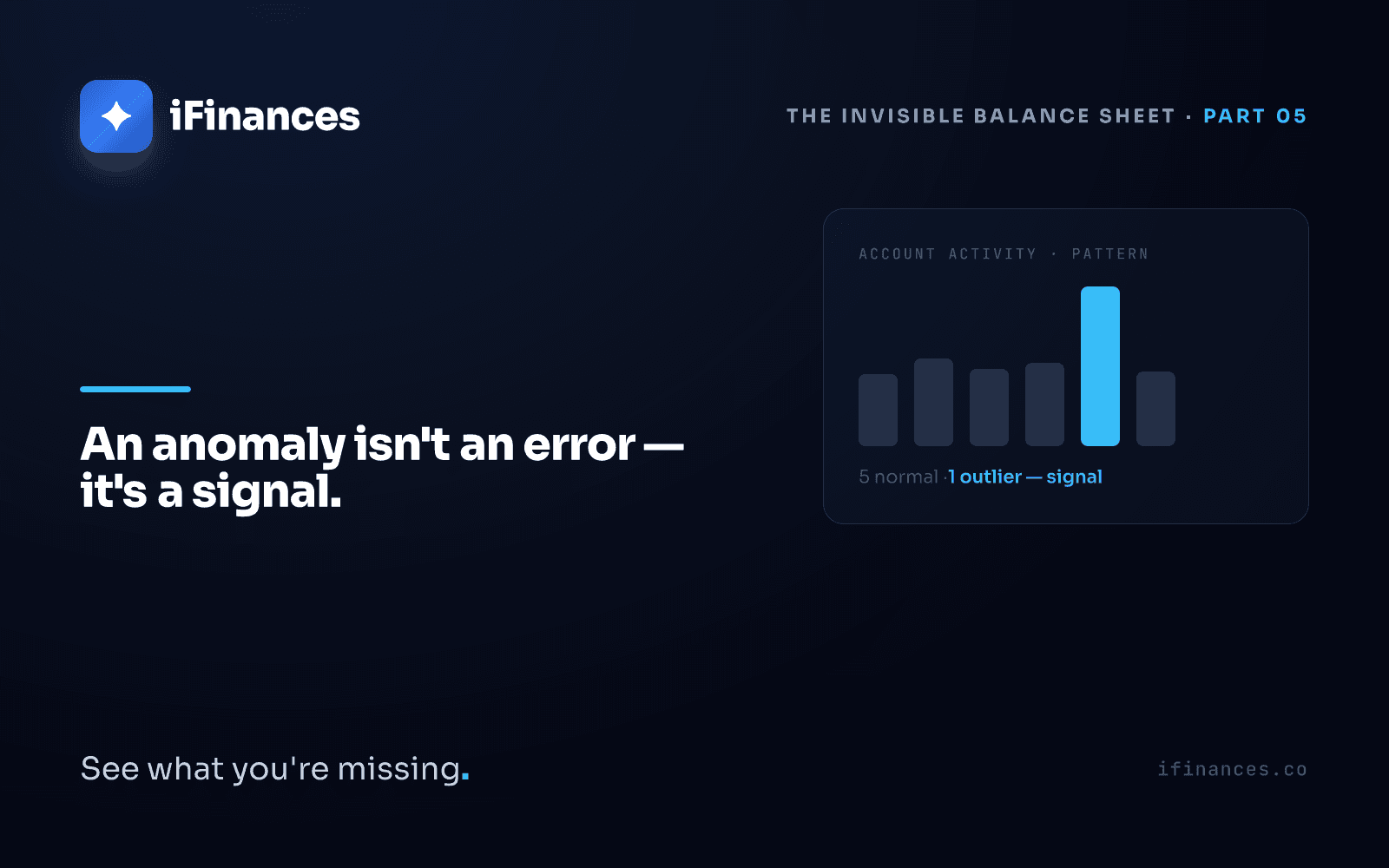

- [Anomaly detection](/en#anomali) flags the line that departs from the pattern — it derives each account's own "normal" and brings what deviates from it to the surface. It doesn't delete an outlier; it shows it to you and says, "look here."

What the three share is this: none of them decides for you. They handle the certain, flag the ambiguous, and leave the rest to you. We don't describe the product as one that "solves," because it doesn't — it shows, makes visible, surfaces. The decision is still yours.

A concrete example: a 1.6 million "open" receivable

Let's not stay abstract. On a mid-sized manufacturer's aging report, one customer carries a 1.6 million lira receivable that has passed 180 days. The collections team is on it; the customer has been called three times, and a draft demand letter is ready. Each time, the customer says the same thing: "We paid this a long time ago."

The statements come out. The customer is right. The money arrived — not in one go, but in three separate payments. The customer closed that 1.6 million invoice in three installments. Accounting recorded each payment faithfully: money in, money in, money in. The invoice also sits on the books. Four lines, all four correct.

The only thing missing is the link between those four lines. None of the three payments was tied to the invoice it belonged to. There is no debt here; there is an unbuilt link. Once the links are built — once the three payments match the invoice they belong to — the remaining amount drops to zero, and the red line in the aging report disappears. Because there was never a real debt underneath it.

What iFinances does is not add a payment your ledger lacks. It places the payment that was already there next to the invoice it belongs to — and, in doing so, surfaces and dissolves a debt that never existed. A phantom debt survives only as long as no one looks at it.

Frequently asked questions

Is the invisible balance sheet an accounting error?

No, and the distinction matters. An accounting error is a wrong entry: a flipped sign, a missing zero, the wrong account. The invisible balance sheet, by contrast, is the missing link *between* correct entries. The invoice is right, the payment is right; only which payment closed which invoice is written nowhere. An error gets caught by eye one day; a missing link stays invisible until someone matches it. That's why the invisible balance sheet costs far more than a wrong number.

Does iFinances replace my accountant or controller?

No. iFinances flags the tens of thousands of lines that can be matched systematically — the certain as certain, the ambiguous as ambiguous — and surfaces the routine. What remains, the handful of lines that genuinely require judgment, it leaves to a human. The goal isn't to replace the accountant; it's to free them from thousands of mechanical decisions and focus them where the real decision needs to be made. The final word always belongs to the accountant.

Do you change my data?

No. iFinances does not rewrite your ledger, add a payment that isn't there, or delete an amount. It sets the records that are already present — your ledger, the e-invoice, the bank statement — side by side and shows the link between them. If a phantom debt dissolves, it's not because we added something, but because we made the real situation visible.

Ready to see what you're missing?

If you sign "balanced" at close while privately wondering "did we, though?" — that "did we" is your invisible balance sheet. Rather than noticing it one day, surface it today: get in touch with us and let's see together what your ledger already says but can't show.

✦ iFinances — See what you're missing.

One post a month.

Get new insights straight to your inbox. No spam, just well-crafted reads.