It's Friday afternoon, two days before the period close. A controller is scanning the bank statement and snags on one line: a customer who pays 40,000 every month has, this month, sent a single receipt of 118,000. The figure isn't round, the description is blank, and it doesn't sit against any invoice.

Your first instinct is familiar: "Probably a mix-up. Let me park it for now, get the close done, and look at it later." You want to lift your hand off that line and move on.

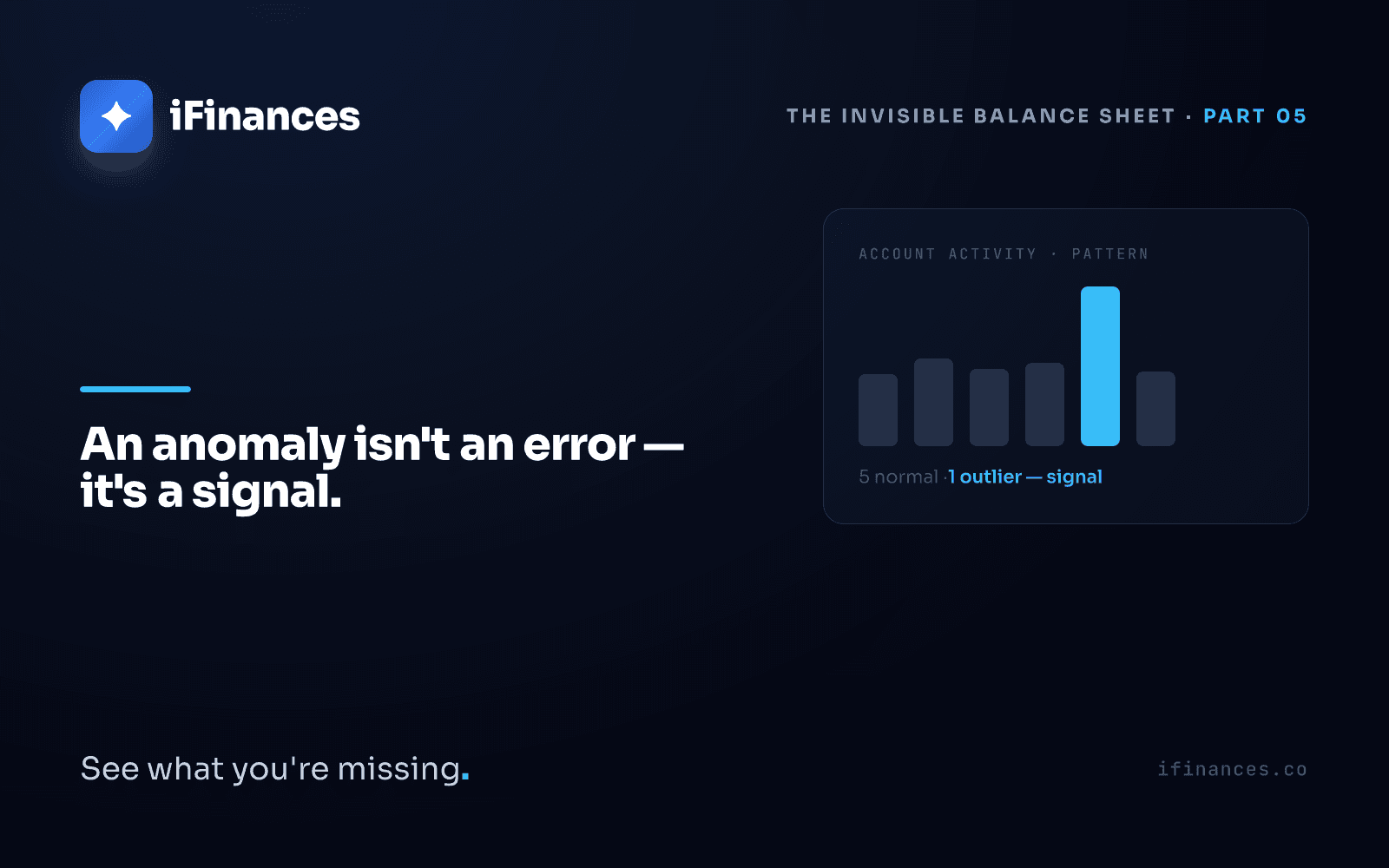

Stop. That line isn't an error. It's telling you something.

This article is built around exactly that reflex. Because a financial anomaly — a record that deviates from the pattern, from what's usual — turns up regularly on the desk of nearly every finance team that deals with reconciliation, account audits and period close. And most of the time it's met with the wrong question: "How do I fix this?" The right question is: "What is this line telling me?"

The mindset shift: not "fix this line" but "what is this line telling me?"

When you meet an outlier record, there are two roads. The first is to treat it as a blemish: correct it, hide it, save the close. The second is to read it as a message: why doesn't this line look like the others?

The difference sounds small, but the consequence is large. An anomaly, on its own, is neither good nor bad. It's neutral. It only says, "something happened here that differs from what was expected." Whether it's good or bad depends on what sits behind it. And you only learn what sits behind it if you ask instead of delete.

A deleted anomaly disappears quietly. A questioned anomaly becomes a finding.

This distinction isn't a matter of personal diligence; it's a matter of institutional habit. A "park it, look later" culture produces a heap of accumulated uncertainty at period end. A "question it, flag it, resolve it" culture produces a ledger that closes clean every month. The only thing separating the two is how you look at the outlier line.

The language of outlier lines: what each type points to

Financial anomalies aren't all one kind. Let's separate a few familiar types and what each one usually heralds. Every item below is a real pattern that shows up often at the reconciliation table:

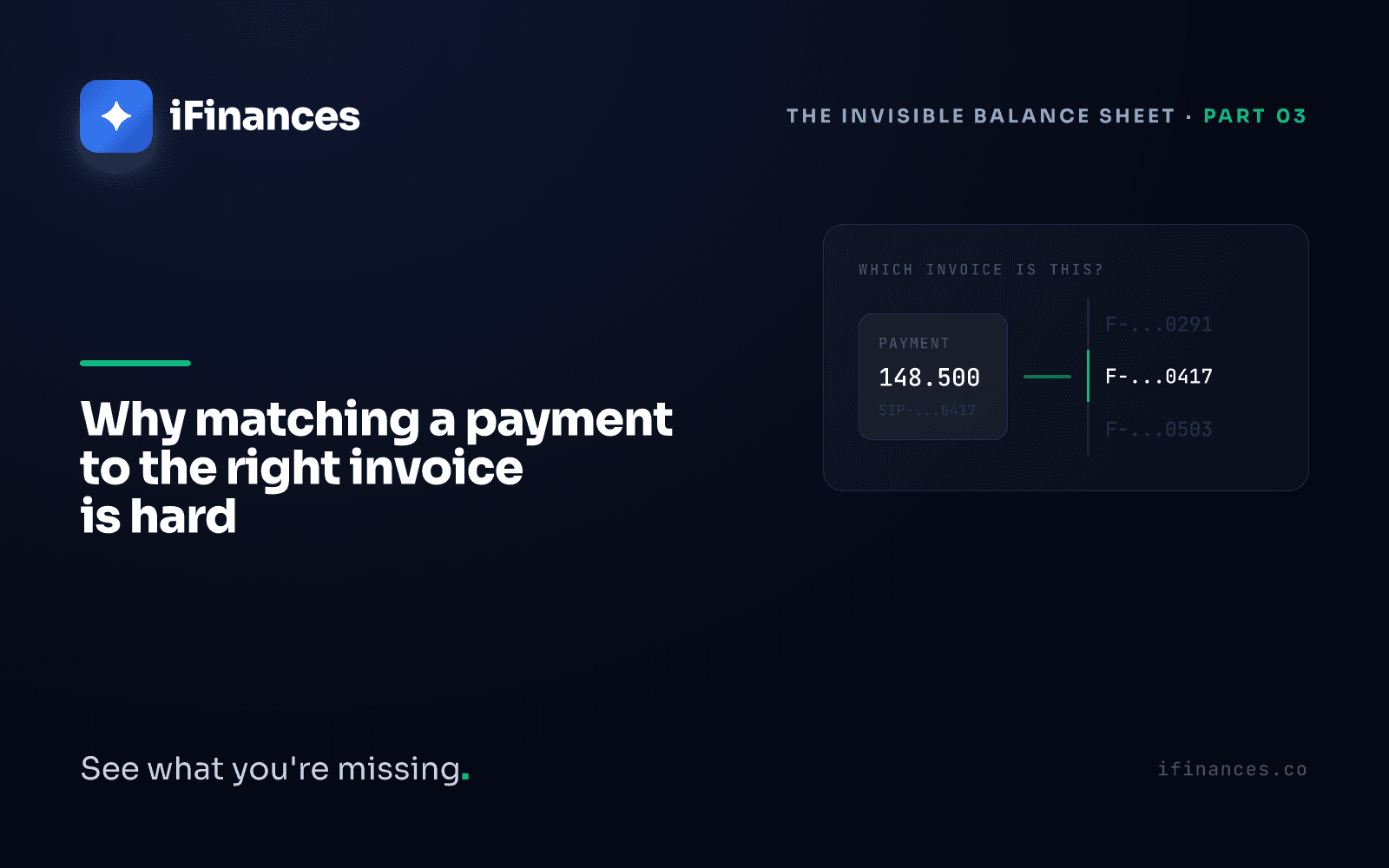

- A payment whose amount deviates far from expectations. A customer who paid 40,000 for months sends 118,000. Most often this signals that several months' or several invoices' worth was paid in one transfer — a single receipt actually closing multiple invoices. But the same deviation can equally signal a transfer that went to the wrong account. The signal is identical; the meaning clarifies only when you look behind it.

- A repeated or duplicate record. The same amount, the same day, almost the same description, twice. This is usually a data-entry error — the same receipt entered twice. Left unseen, you'll believe you have a receipt that doesn't really exist, and appear to have closed a receivable a customer never owed.

- A receipt that matches nothing. Cash landed in the account but couldn't be tied to any invoice — this is called unapplied cash (a receipt never posted against an invoice). It usually points to a process gap: the payment arrived, but where it belonged was never noted anywhere. It looks minor; accumulated, it forms a pile on the balance sheet where "whose, and against what" is anyone's guess.

- Unusual timing. A customer who always pays on the 5th sends payment on the 26th, or a flurry of adjustments clusters right before the period closes. Timing alone isn't a defect; but timing that departs from the pattern justifies the question, "a human intervened here — why?"

- The wrong currency. A single foreign-currency item surfacing in an account — that is, the running record of reciprocal debits and credits with one customer — that has always run in local currency. This could be a booking error, or a genuine FX transaction that slipped past unnoticed. Either way, left untouched, it quietly misstates the balance.

Notice: for none of these types do we say "this is an error in itself." Each opens a range of possibilities — a process gap, a double count, a lost invoice, an ordinary human slip, or, rarely, misuse. The anomaly's job isn't to hand you a conclusion; it's to place the right question in front of you.

An anomaly and missing data are not the same thing

Let's separate a common confusion here. A record being *missing* and a record being *anomalous* are different things. How situations like missing invoices, duplicate records and orphaned receipts arise and surface is covered in detail in financial anomaly detection — missing invoices and duplicates. This article's subject is narrower and more cognitive: which eye you bring to the outlier line.

How they're caught: not by scanning line by line, but by flagging the deviation from the pattern

A human scanning ten lines senses the odd one. At a hundred lines, they struggle. Across tens of thousands of lines, six companies and two currencies, that intuition is exhausted entirely — because it's no longer possible to hold in your head what "normal" even is.

This is where anomaly detection — flagging the unusual pattern as a signal rather than an error — comes in. The logic here isn't to look at each line and ask "is this correct?" It's first to derive each account's own normal: how much, how often, and in which currency does this customer typically pay? Then to surface what deviates from that normal. The human doesn't audit every line; the system brings the human the small number of lines that actually warrant attention.

For an accountant, that means simplification: instead of eye-scanning thousands of records, they devote their attention to the handful of lines that genuinely require judgment. The system says "this line is unusual"; the decision "what does it mean and what should be done" stays with the person. The aim isn't to replace the accountant; it's to leave them the judgment work only a person can do.

The system shows which line to look at; a person still decides what that line means.

This is how iFinances' anomaly detection module works at its core. The system derives a "normal" profile from each account's own history; when payment amount, frequency, currency and timing deviate from that profile, it flags the line. A flagged line isn't an accusation, it's an invitation: "take a look here."

Not a black box, but a chain of reasoning

Flagging a line as "anomalous" isn't enough on its own. For a finance manager or an auditor, the real question is: *why* was it deemed anomalous? Without an explainable rationale — "this customer typically pays once a month, averaging 40,000; this record is both three times larger and on an unusual day of the month" — the flag doesn't inspire trust. Why it's essential to present the reason an anomaly counts as a signal through a traceable chain of reasoning is something we address in explainable AI: black box vs. reason chain. In short: flagging is easy, *justifying* is valuable.

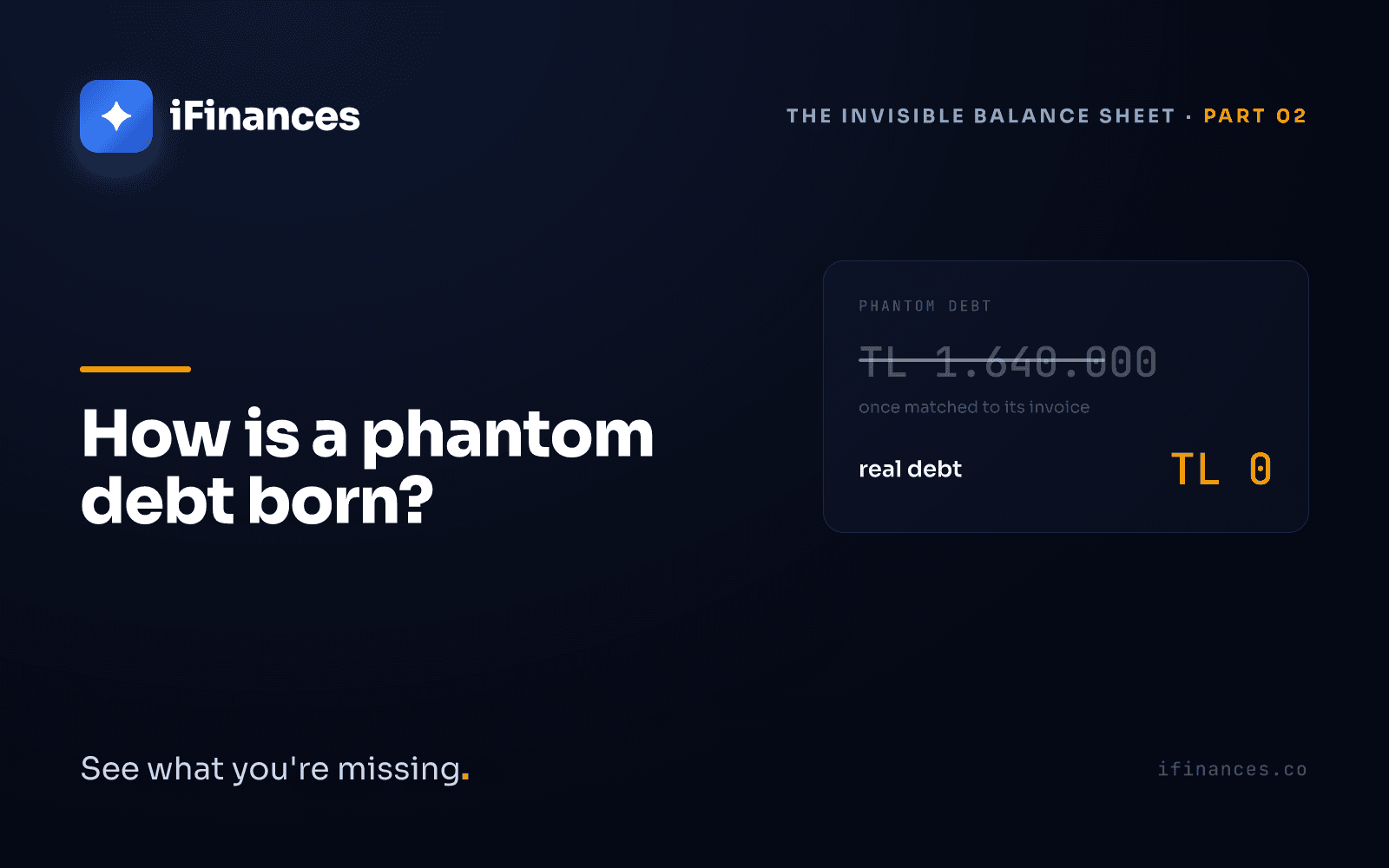

The link between anomalies and phantom debt

One of the costliest kinds of anomaly is born from the "matches nothing" category. A payment lands in the account but isn't tied to any invoice. It's visible on the record side; it's invisible on the relationship side.

Its mirror image is another anomaly running in the opposite direction: a paid invoice still showing "open" in the ledger. We call this phantom debt — a receivable that doesn't actually exist but keeps living in reports because no match was made. How a phantom debt arises, how it inflates the aging report, and how it turns into a double-collection risk is walked through step by step in phantom debt: why a paid invoice shows as open.

Consider the two together: unapplied cash is "there's money, no invoice"; phantom debt is "the invoice is open, no payment attached." Both are different faces of the same root cause — an unmade connection. And both, read correctly, are anomaly signals. That's why thinking about anomaly detection alongside matching matters; our matching approach, which systematically sets payment and invoice side by side, resolves most anomalies before they're even born, leaving only the minority that genuinely require judgment.

An anomaly seen early is a note; seen late, a surprise

That same 118,000 line has two possible fates.

Spotted on Friday afternoon: a two-minute check, a note reading "yes, three months' payment arrived in one shot," three invoices closed correctly. A small correction, a clean close.

Not spotted, parked and forgotten: three months later that customer calls, says "we paid those three invoices," and you still show two of them open on your ledger — perhaps you try to collect one again. What could have been a small note turns, at period end, into a surprise, a snag in a customer relationship, a double-count risk.

The only difference between the two is that the line was read instead of deleted.

This also shows why reconciliation is a continuous discipline, not an "end-of-month chore." When you catch the anomaly early, you bring the reconciliation table where you sit down with the other party not uncertainty but resolved lines. E-reconciliation — the electronic reconciliation system run by Turkey's Revenue Administration, whereby two parties compare and confirm their total balances electronically — tells you whether the total agrees; but it doesn't show whether the lines beneath the total genuinely match. The anomaly, more often than not, emerges at exactly that line level.

Turning the anomaly into a culture

Reading an anomaly correctly isn't a one-off skill, it's an institutional habit. In practice it reduces to three steps:

- Flag it, don't delete it. Keep the outlier line visible instead of hiding it. "Parking" a record to get the close done isn't resolving it — it's deferring it.

- Ask, don't assume. Before saying "probably an FX difference" or "probably a mix-up," verify the event behind the line. An assumption is cheap; a wrong assumption costs dearly months later.

- Resolve it, leave a note. Every flagged line should be tied to an outcome — closed, explained, under review — and that decision should remain as a traceable note. That way the same anomaly isn't argued from scratch next period.

These three steps work the same way on a single accountant's desk and in a finance team consolidating six companies. What iFinances does is make this discipline sustainable at scale: it surfaces what deviates from the pattern, shows the rationale, and leaves the decision to you. You can see how the product's reconciliation, matching and anomaly modules work together in the module overview.

Frequently asked questions

Is a financial anomaly always an error?

No. An anomaly is neutral — it only says "something happened that differs from expectations." An outlier line can be a legitimate receipt closing several invoices at once, or a transfer sent to the wrong account. Its meaning clarifies only when you look behind it. That's why the right reflex isn't to delete but to ask. The anomaly's job isn't to hand you a conclusion, but to place the right question in front of you.

Does anomaly detection replace the accountant?

It doesn't. The system shows which line deviates from the pattern and why it deviates; but the decision "what does it mean and what should be done" stays with the person. The aim is to free the accountant — who would otherwise eye-scan tens of thousands of lines — from mechanical checking and turn their attention to the small number of lines that genuinely require judgment. The routine surfaces; the decision stays human.

What's the difference between unapplied cash and phantom debt?

Unapplied cash is the "there's money, no invoice" case: a receipt that landed in the account but was never tied to any invoice. Phantom debt is the reverse: an invoice that has been paid but, because it was never matched, still shows as "open" in the ledger. Both are different faces of the same root cause — an unmade connection — and both are anomaly signals.

If you'd like to surface, together, the outlier lines your ledger already contains but can't show you, get in touch with us.

✦ iFinances — See what you're missing.

One post a month.

Get new insights straight to your inbox. No spam, just well-crafted reads.