Two finance teams sit across a table. Both hold the same account — the shared ledger of what each owes the other — yet they read two different numbers. Your books say 1,240,000. The other side says 1,180,000. That 60,000 gap looks, at first, like a question of "who's right?" It isn't. That 60,000 is the name for something neither side can see in the moment: the same payments and the same invoices, tied together differently in two separate ledgers.

Then the familiar traffic begins. Hours of phone calls, statements shuttled back and forth, sentences like "you've closed that invoice, but we still see it open." Eventually the numbers agree, both sides relax, the reconciliation letter is signed and filed. But what exactly did you just do? You didn't complete an arithmetic exercise. You rebuilt trust.

This article is about why that scene — repeated hundreds of thousands of times a month — deserves to be treated not as a spreadsheet chore but as trust infrastructure between companies. And why a ledger that reconciles down to the line means cash, time, and reputation for any CFO or controller.

Reconciliation is a relationship, not a calculation

In most companies, reconciliation is filed under "month-end chore." Pull the list, send it to the counterparty, force the numbers to match if they don't, sign, file. That framing reduces reconciliation to a formality — a box ticked, a requirement met. What it actually does is far more foundational.

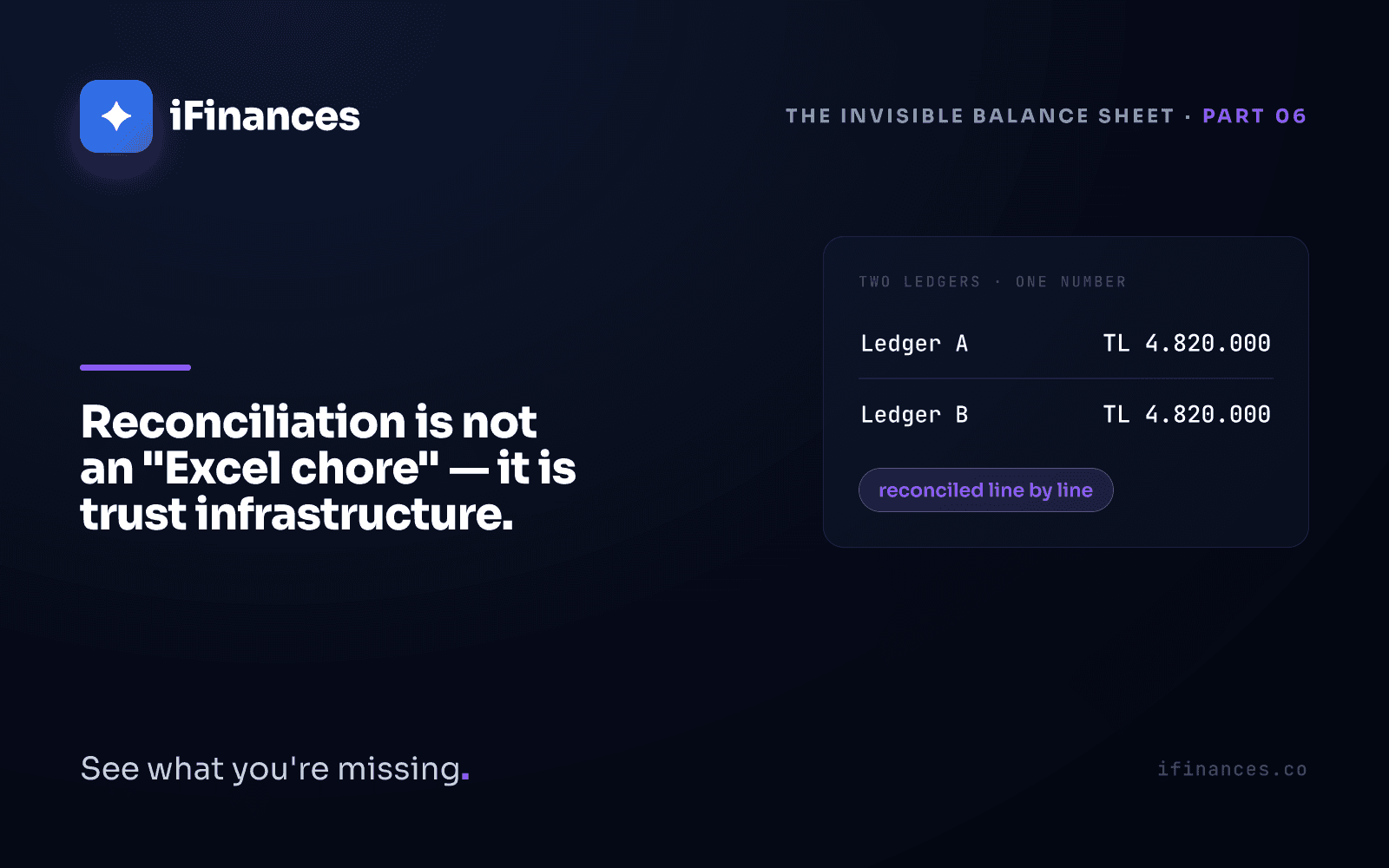

Reconciliation is the point at which two parties' accounts agree. But "agree" is deceptively simple. The real work isn't equalizing two numbers; it's getting two companies to agree on the same sequence of events. Which invoice was issued, which payment arrived, which payment closed which invoice and by how much. When both sides reach the same figure, they've actually met on the same version of the past.

Agreeing on a number is easy. Agreeing on the same story is hard — and that's the part that matters.

This is why reconciliation is as fundamental as a contract or an invoice. The contract starts the relationship, the invoice documents the claim, and reconciliation confirms — to both sides at once — where the relationship stands today. All three are infrastructure for commercial trust. Yet only one of them — reconciliation — gets mistaken for busywork and never earns its place. Lawyers guard the contract; regulation guards the invoice; reconciliation gets squeezed into a hand-forced spreadsheet at month-end, under closing pressure.

Balance reconciliation and account reconciliation are not the same thing

Two concepts get blurred in practice. Balance reconciliation compares only the final figure — "what you show, what we show." Account reconciliation confirms that the movements behind that balance — the invoice and payment lines — sit the same way on both sides. The first checks the outcome; the second checks the process. As the next section shows, trust lives in the second — because a dispute never surfaces in a total. It surfaces in a line.

e-Reconciliation confirms the total. Trust lives in the line

E-reconciliation — the electronic process by which two counterparties compare and approve their balances through a shared platform — does real work here. It standardizes the manual letter traffic, the signature and delivery process, and makes it traceable. When the totals match, both sides declare themselves reconciled and the process closes. That's a substantial step up from chasing reconciliation letters one email at a time. We cover what e-reconciliation is, how the process runs, and how the balance shifted after the old declaration forms were retired in a separate piece: e-reconciliation, the tax-authority process, and the post-form landscape.

But there's a critical distinction. The total matching does not mean the story matches.

Two companies can meet perfectly at the same 1,180,000 — one arriving there by treating three invoices as closed, the other by treating two as closed and one payment as not yet matched. Same total, different reality. E-reconciliation confirms the aggregate balance; it doesn't show the line-level detail of which payment closed which invoice. Both sides look reconciled, while underneath sit two different stories.

The real trust hides in that line. Because disagreement never surfaces in the total; it always surfaces in a line.

- "That invoice we paid in March" is a line.

- The customer your collections team calls unnecessarily three months later is a line.

- The item an external auditor opens and asks "why is this still outstanding?" is a line.

- The dispute two periods later, when the counterparty says "we already cleared that amount," is a line.

Two companies that look reconciled on the total but don't agree at the line haven't reconciled — they've deferred. The only question is when, and how large, that deferred bill will arrive.

Why it's strategic: a reconciled ledger is a ready ledger

For a CFO or an owner, the value of reconciliation goes well beyond the relief of "the numbers matched." A ledger reconciled at the line level says three concrete things at once.

1. You're audit-ready

When an external auditor asks about an outstanding receivable, how it was closed — or why it's still open — must be traceable. In a line-reconciled ledger that answer is already there; you don't go hunting when the question comes. That difference is the essence of being continuously ready for audits — keeping the ledger in a self-defensible state instead of scrambling to prepare each period-end. We walk through the operational side of this step by step in audit-ready reconciliation for external audits.

2. Your collections are clear

Who actually owes money, and whose balance only *looks* "open" because it hasn't been matched — line-level reconciliation separates the two. Collections stop chasing debts that don't exist and stop overlooking risks that do.

The danger here has a name: phantom debt. Money that was paid, but whose payment was never matched to the relevant invoice, so it still shows as "open" in the ledger — a debt that doesn't exist in reality. It turns red on the aging report, drops onto the collections list, distorts the cash-flow forecast — while there was never a real receivable underneath it. We explain how a phantom debt is born, how it grows on its own, and how invoice-payment matching dissolves it in ledger record versus reality: the invisible balance sheet.

3. Your disputes are few

When both sides agree on the same lines, the "we already paid this" phone call three months later either never rings or closes in a minute. You don't renegotiate every reconciliation round from scratch, because the past sits the same way in both ledgers.

None of this is accounting elegance or aesthetic rigor. It translates directly into cash, time, and reputation. A company can be run on an unreconciled ledger — but it's run on top of an unseen uncertainty. And that uncertainty tends to surface at its most expensive point, at the least expected moment.

An unreconciled ledger may not be wrong. But it's ground you're standing on without knowing it holds.

Trust infrastructure can't be carried by eye

The defining property of trust infrastructure is that it works at scale without breaking. A bridge has to be safe not for ten cars but for tens of thousands. Reconciliation carried by hand cracks exactly here.

Ten or a hundred invoices can be reconciled manually. But across tens of thousands of lines, multiple companies, two currencies, with four separate complications stacked on top of each other, the work exceeds what one person and one spreadsheet can carry:

- Partial payments. A customer pays one invoice in three installments, or three invoices in one transfer; which amount closes which remainder?

- FIFO closing discipline. FIFO — "first in, first out," the rule of closing the oldest open invoice first. A manually tracked sequence slips somewhere; an old paid invoice shows open, while a newer one appears closed ahead of its due date.

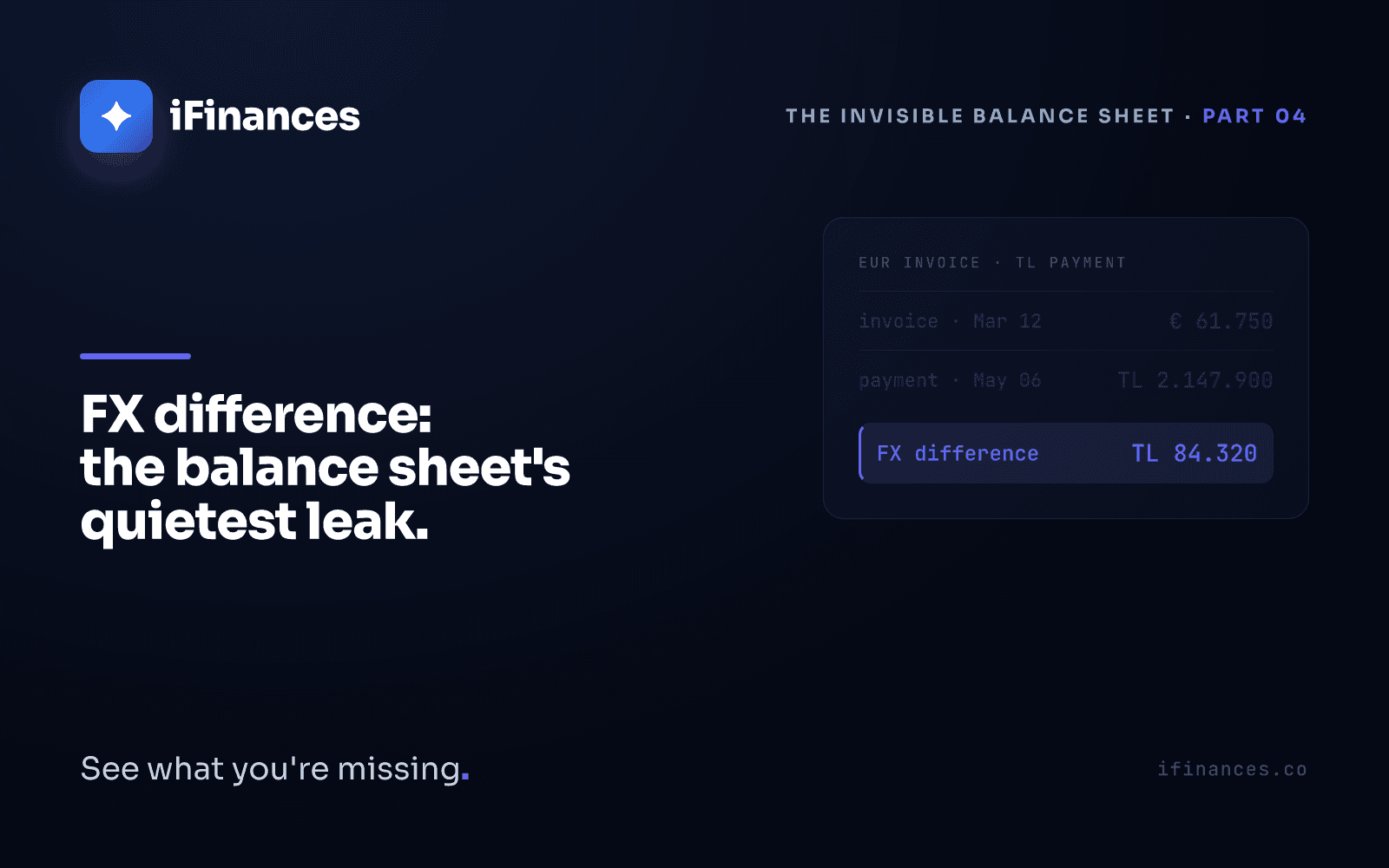

- Cross-currency FX differences. A foreign-currency invoice is closed by a local-currency payment on a different date. The difference arising from the exchange-rate movement between the two dates — a cross-currency close, where the invoice's and the payment's currencies diverge — has to be judged: is it a reasonable FX difference, or an inconsistency worth investigating? Doing that by eye across hundreds of invoices isn't sustainable.

- Unidentified transfers. A bank description carries an order number but no company name. The money arrived, but because "whose?" stays unanswered, it attaches to no invoice. This is unapplied cash: money collected but never posted against an invoice.

When these pile up, the result isn't a *wrong* ledger — it's an incomplete one. The total holds; the lines don't. And trust infrastructure can't be left to eyeballing and good intentions; it has to be systematic and transparent. Why each line arrived at its figure must be traceable backward.

This is precisely why reconciliation becomes a software question — but which software? The right tool has to center not aggregate matching but line-level traceability. We collected the criteria to weigh when choosing a reconciliation tool in reconciliation software selection: 7 critical criteria.

Automation doesn't replace the accountant. It clears room for them

A misunderstanding is worth dispelling up front. The aim of systematic reconciliation is not to displace the accountant or controller. Quite the opposite: the thousands of lines a machine matches consistently let the human eye turn to the minority that genuinely requires judgment. The routine surfaces; the decision remains.

The iFinances matching engine marks the certain as certain and the uncertain as uncertain; it ties each payment to the invoice it belongs to based on company, amount, and date, applies FIFO discipline on partial payments, and reads the reference embedded in the description. But when a reference is ambiguous, an amount falls outside a reasonable FX band, or a pattern is unusual — anomaly detection surfaces these as a signal and leaves the decision to the human. The system says "this line needs a look"; the "what does this mean and what should we do" call stays with the professional. The point is to lift the drudgery of tens of thousands of mechanical decisions and focus attention on the judgment only a person can supply.

The invisible balance sheet, when it becomes visible

Across this series we've seen the same layer each time. In a phantom debt, in the matching that ties a payment to an invoice, in a cross-currency FX difference, in the anomaly detection that treats an unusual pattern as a signal rather than an error — in every case, what spoke wasn't the records themselves. The relationship between the records spoke. That's the layer we call the invisible balance sheet: the layer the ledger doesn't lie about but can't display.

When that layer becomes visible, reconciliation stops being a chore. Two companies meeting on the same figure is no longer a total forced together at month-end but a reconciliation with line-by-line grounding. In other words, trust. The iFinances reconciliation module is built precisely to make that line-level grounding visible — which payment closed which invoice, and why. You can see the product as a whole on the modules overview.

We built iFinances for exactly this. Not to rewrite your ledger, but to surface the relationship your ledger already states. Because when two parties agree on the same figure, what happens isn't arithmetic. It's trust. And trust carries value only when it's visible.

Frequently asked questions

If I've done e-reconciliation, why do I need line-level reconciliation?

E-reconciliation compares and approves the two parties' total balance electronically — the version of reconciliation settled into process and compliance. But the total matching doesn't mean the movements beneath it match. Two companies may reach the same balance through different invoice-payment matches. Line-level reconciliation answers "which payment closed which invoice," and because disputes and audit questions always surface at the line, that's where real trust lives.

Does line-level reconciliation eliminate my accountant's job?

No. Systematic matching takes on the repetitive, mechanical decisions across tens of thousands of lines — the certain matches, the FIFO sequence, the clear references. It flags the lines that stay ambiguous, fall outside a reasonable FX band, or deviate from the pattern, and leaves them to a human as a signal. It doesn't replace the accountant; it frees them from drudgery and focuses them on the judgment only a person can supply — resolving a dispute, interpreting a pattern.

What difference does a reconciled ledger make for audit readiness?

An external auditor typically asks why a receivable is still open, or which invoice a collection closed. In a line-reconciled ledger the answer is already recorded; there's no scramble for documents, no reconstructing the past. That means the ledger stays continuously defensible rather than requiring a separate preparation rush each audit period — an audit-ready structure.

---

If you'd like to see whether your ledger reconciles on the total but comes up short at the line, get in touch; we'll show you what's already visible in your own data.

✦ iFinances — See what you're missing.

One post a month.

Get new insights straight to your inbox. No spam, just well-crafted reads.