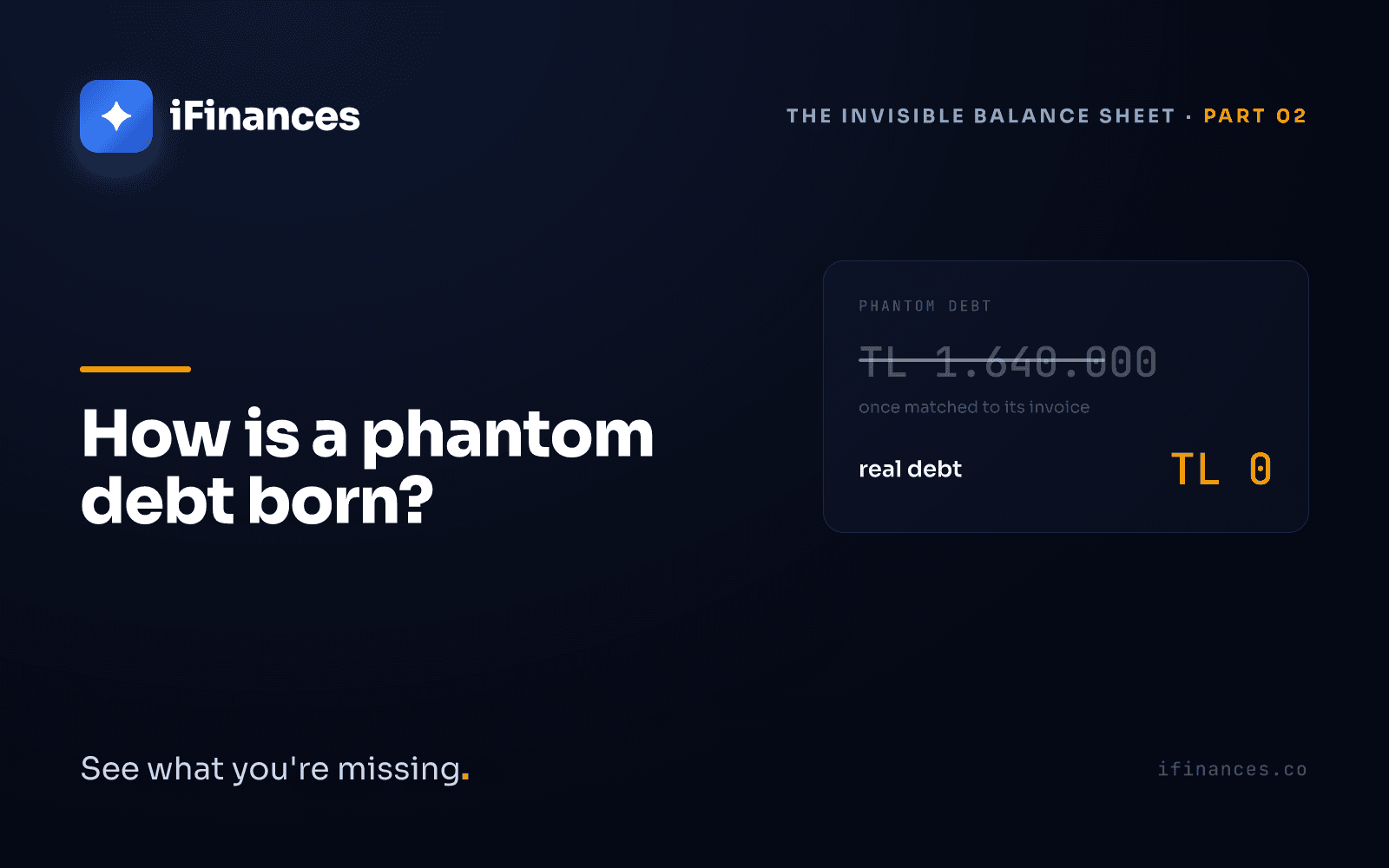

On a Monday morning, the finance lead at a mid-sized manufacturer opens the aging report. An aging report is the table that shows how long receivables have stayed open: 30, 60, 90, 180 days. Against one customer sits an open receivable of 1.6 million, past 180 days. The collections team is already on it; the customer has been called three times, and a demand letter draft is ready. Each time, the customer says the same thing: "We paid that a long time ago."

The bank statements come out. The customer is right. The money arrived, and not in one go either, but across three separate payments. So why does the ledger still show 1.6 million as open?

That debt was never wrong. That debt never existed.

We call this phantom debt: a debt that has been paid but appears "open" because the payment was never matched to its invoice, a debt that does not actually exist. Once it is born, if no one stops it, it grows on its own and lives in your ledger for weeks or months as if it were a real risk. This article breaks down the anatomy of that silent number in three stages, for CFOs, controllers, and accountants who deal with reconciliation and receivables tracking: how it is born, how it grows, and how it dissolves.

What is phantom debt? Not a wrong number, a missing one

The error companies talk about most is the visible one: a mistyped amount, a flipped sign, an extra zero. These errors are noticed and corrected sooner or later, because something "doesn't add up" somewhere. A total comes out wrong, a balance looks nonsensical, and someone stops to look.

Phantom debt is not that kind of error. That is exactly what makes it dangerous.

Phantom debt is not wrong; it is incomplete. The number looks internally consistent, the balance sheet still ties out, and no alarm goes off.

There is no incorrect entry anywhere. The invoice was issued, at the right amount. The payments landed in the account, at the right amounts. Examined line by line, every row is flawless. The only thing missing is the link between those rows: which payment closed which invoice, and by how much. We call this link invoice-payment matching, the work of tying a payment to the invoice it belongs to, on the basis of amount, date, and counterparty. Until that link is made, a payment sits there as "cash received" and an invoice sits there as "open receivable," separately. You only realize they are the same transaction once someone matches them.

This is why phantom debt outlives a classic accounting error by so much. A wrong amount will catch your eye one day. But no total gives away a missing link, because the total is already correct. The gap is not inside the rows; it is between them.

Birth: the moment the link is not made

A phantom debt is born not from an error but from an omission. The moment it is born is the moment a payment fails to meet its invoice.

Back to our example. The customer closed that 1.6 million invoice with three payments. The first does not cover the full amount; the second arrives; the third completes the remainder. Accounting faithfully records each payment: money in, money in, money in. The invoice sits in the records too. Four rows, all four correct. The only thing missing is the link between them.

In a multi-payment closure, that link can break in three separate places. Each one creates a different kind of invisibility in your ledger.

- One payment is posted to the wrong invoice. That other invoice is over-closed, while ours still shows open. The money went into the right account, but was let in through the wrong door.

- One payment is posted to no invoice at all. The bank memo carries an order number but no company name; the question "whose money is this?" goes unanswered, and the payment sits idle. This is called unapplied cash: money that has been collected but never applied to an invoice. It shows on the statement, but it closes no debt on the receivables list.

- After a partial payment, the remaining amount looks like the full balance. Without the discipline of closing the oldest open invoice first, a rule we call FIFO ("first in, first out"), the paid portion melts away somewhere and the invoice stays open at its original full amount.

In all three, the outcome is the same: the money entered your account, but the ledger does not see it. The entry is correct; the relationship is missing. Phantom debt is born in exactly this gap.

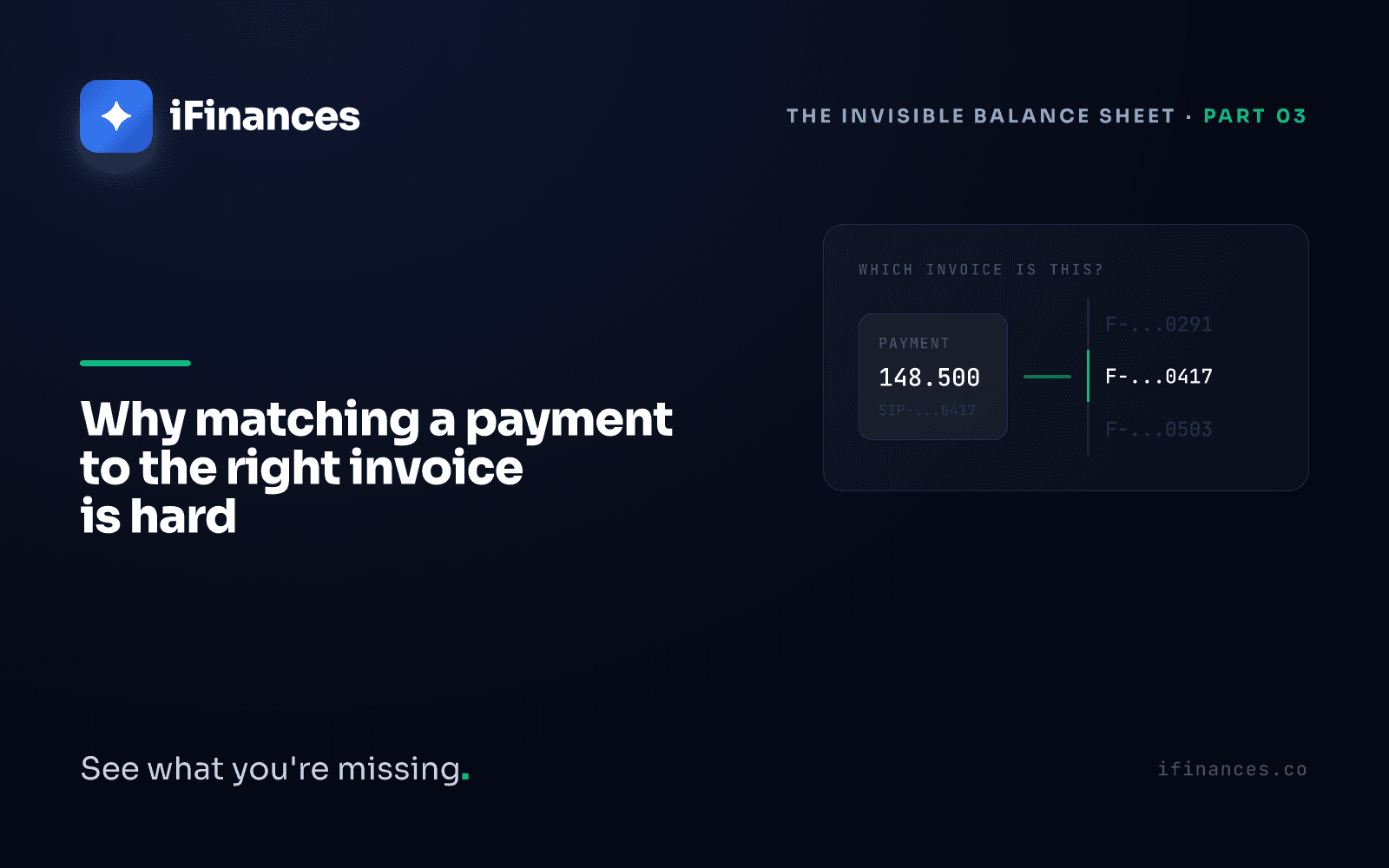

Why multi-payment closures are especially risky

When one payment arrives against one invoice, making the link is easy: the amounts match, the dates are close, the counterparty is clear. Partial payments and multi-payment closures, on the other hand, create a chain. At every link in the chain there is a new question: How much of the invoice did this payment close? How much remains? Should the next payment come off the remainder, or off another invoice? Holding the answers to these questions across tens of thousands of rows, several customers, and two currencies goes beyond what a person can carry. We cover why matching a payment to an invoice is harder than it looks in a separate piece, with the anatomy of partial payments and FIFO ordering. For now it is enough to know this: phantom debt is most often born when one link in that chain quietly snaps.

Growth: the report mistakes it for real

The dangerous part of phantom debt is not its birth but its silent growth. At birth it is innocent and easy to fix. The problem is that no one looks at it.

Once it is recorded as "open," that amount marches through the aging report period after period. 30 days, 60 days, 90 days. With each close it ages a little more, turns a little redder. No one touches it, because the system presents it as a genuine receivable. And because it looks like a genuine receivable, it produces genuine consequences.

Then the chain reaction begins:

- Collections chases it. To ask for money that does not exist, they call the customer, exchange emails, prepare a demand letter. Every hour spent is stolen from time that could go to a real receivable.

- Tension builds with the customer. The other side knows they paid; you say they didn't. Every call erodes a little of the trust you built over years. A reconciliation dispute is often not an accounting problem but a relationship problem.

- The cash-flow forecast breaks. You say "we're expecting this much in collections," when that money has long since arrived. Your expectation of the future is built on a line item closed in the past. The cash you planned for is already sitting in your account.

- The worst case is double-counting. If the customer, in good faith, says "fine, let me pay again," you collect the same receivable twice. That is no longer a recording artifact; it is a real cash movement that has to be corrected. And correcting it is far more expensive than the debt was to create.

A wrong amount gets caught by eye one day and corrected. Phantom debt is not wrong, merely incomplete. And you lose time, reputation, and a sound basis for decisions chasing a debt that isn't there.

For the CFO and the accountant, this is where the real issue knots together. If a phantom debt sat alone in one corner of your balance sheet, its cost would be limited. But remember that a balance sheet works like an organ: the aging report feeds the collection plan, the collection plan feeds the cash projection, and the cash projection feeds investment and payment decisions. A single phantom number at the head of the chain seeps into all of those decisions. You cannot collect a receivable you don't see, you cannot manage a risk you don't see, and you cannot make sound decisions on a phantom debt you don't see, yet you still make decisions on that number.

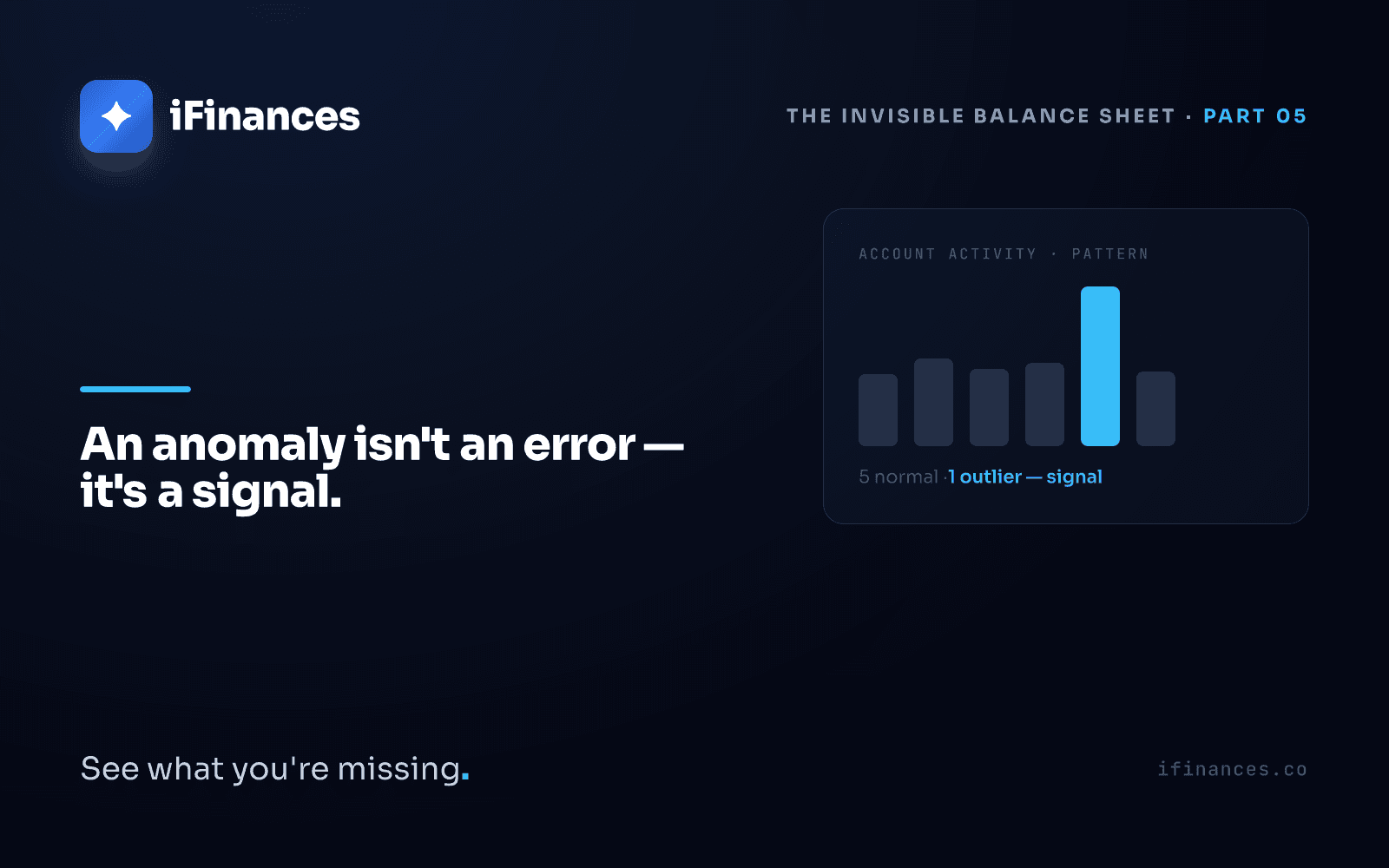

Phantom debt may be a systemic pattern, not a single anomaly

A phantom debt rarely comes alone. The process gap that produced it usually produces the same gap for other customers. If a "payment with no company name in the memo" went unmatched once at a company, it has probably gone unmatched dozens of times more. So fixing a single phantom debt is not enough; you have to surface the pattern that produces it. We separately address what kind of systematic approach it takes to read irregularities like missing invoices, duplicate entries, and stranded collections as signals, in our piece on financial anomaly detection. In short: a phantom debt is not an error but a signal; and signals usually come in plurals.

Dissolution: matching brings it to the surface

Phantom debt dissolves the moment it is seen. Because it is not a debt that truly exists. The only thing keeping it alive is that no one looks at it.

The way to make it visible is not to pick through rows by hand. It is practically impossible for a person to scan tens of thousands of rows by eye and find the missing link; phantom debt is, after all, a child of that impossibility. The solution is to place payment and invoice side by side systematically:

- Tie each payment to the invoice it belongs to, based on company, amount, and date.

- When the memo is unclear, match the order or reference number in the bank memo against your order records.

- On partial payments, close from the oldest open invoice in sequence, with FIFO discipline, so that the destination of the paid portion is recorded.

- Remember that not every credit line on the statement is a customer collection: interest income, FX difference (a revaluation gain or loss from exchange-rate movement), and internal transfers also appear as credits but close no invoice.

When you do this consistently across tens of thousands of rows, that 1.6 million "open" receivable dissolves. The three payments match to the invoice they belong to. The remaining balance drops to zero. The red line on the aging report vanishes, because there was never a real debt beneath it, only an unmade link.

This is not about replacing the accountant

An important distinction deserves emphasis here. Systematic matching does not substitute for the accountant. On the contrary: the thousands of rows the machine matches consistently free the human eye to focus on the minority that genuinely requires judgment. An ambiguous reference, an unusual pattern, a difference that needs explaining. The routine surfaces and dissolves; what remains is only the decision. iFinances carries this distinction as a principle: it surfaces the routine and leaves the judgment to the human.

Indeed, a lasting solution to phantom debt does not end with looking at a single source. The true picture emerges only when three sources, the bank statement, the e-invoice records, and the accounting ledger, are compared at the same time. We explain how three-way cross-reconciliation works in a separate article; there you can see why phantom debt can never be fully resolved by looking at a single source. In brief: a payment exists on the statement but is not linked to its invoice in the ledger; you see that gap only when you place the two sources side by side.

What was invisible, now visible

At the start, the ledger held a 1.6 million debt. It was red on the aging report, on the collections team's list, inside the cash-flow expectation. It looked real. Everyone treated it as real.

What was invisible was that the debt had already been paid. The money had arrived, but none of the three payments had been linked to the invoice it belonged to. There was no debt, only a missing link. And the moment that link was made, the number you had been chasing as "debt" evaporated.

What iFinances does is not add a payment to your ledger that isn't there. It is to place the payment already sitting there next to the invoice it belongs to, and thereby surface and dissolve a debt that never existed. The product's matching engine does this at scale; the reconciliation workbench then shows, on a single screen, which links are solid and which are suspect. A phantom debt lives only as long as no one looks at it.

Frequently asked questions

What is the difference between phantom debt and doubtful receivables?

A doubtful receivable is one that genuinely exists but whose collection is seen as risky; the debt is real, and whether it can be collected is uncertain. Phantom debt is a receivable that does not actually exist: the payment was made long ago and shows "open" in the ledger only because it was never matched to its invoice. One represents a real risk, the other a missing record relationship. For a doubtful receivable you book a provision; for phantom debt you perform matching and the debt dissolves.

Why does a paid invoice still show open?

There are three common reasons. First, the payment may have been posted to the wrong invoice; the money arrived but closed a different debt. Second, the payment may not be linked to any invoice; the bank memo lacks a company name, and the money sits idle as unapplied cash. Third, when FIFO discipline is not applied to partial payments, the paid portion goes unrecorded and the invoice stays open at its original full amount. In all three, the money is in the account; what is missing is the matching that links the payment to the invoice.

How do we detect phantom debts on a regular basis?

Not with a one-off check, but with systematic reconciliation. You need a recurring process that ties each payment to its invoice by company, amount, and date; closes partial payments with FIFO; and cross-compares bank, e-invoice, and ledger. This process also produces a record trail that stays continuously audit-ready; we explain how audit-ready, traceable reconciliation for KGK audits is built in a separate article. Once the process is in place, phantom debts surface not one by one but as a pattern.

If you want to see how much of your ledger is real and how much is a missing link, get in touch with us; let's review together what shows and what doesn't across your current receivables.

✦ iFinances — See what you're missing.

One post a month.

Get new insights straight to your inbox. No spam, just well-crafted reads.