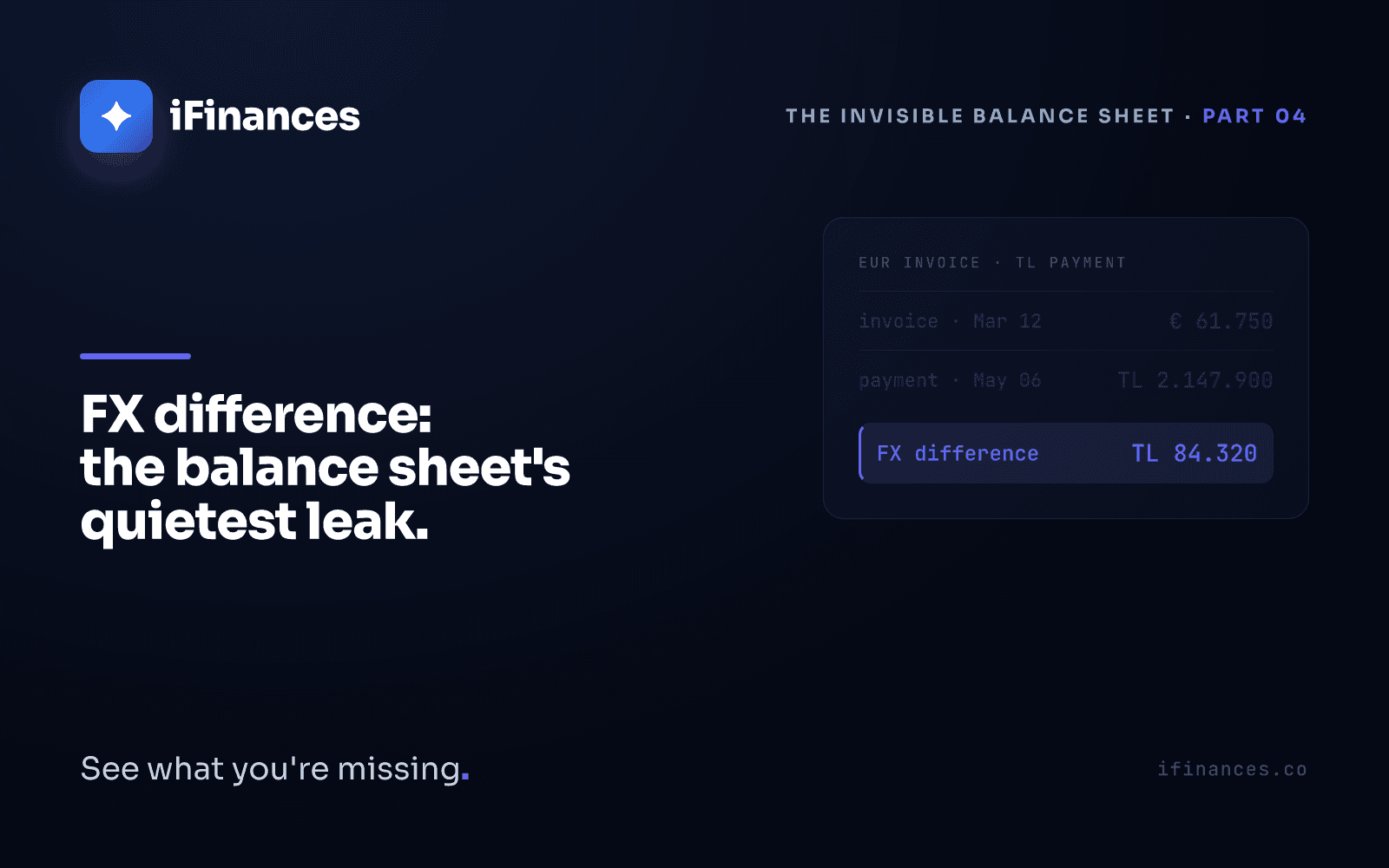

You issued an export invoice: EUR 10,000. Your customer paid two months later, and paid in Turkish lira, at that day's rate. The amount landed in your bank account, the entry was booked, the invoice was marked "closed." When month-end arrived, the balance tied out and everyone signed off.

But on the day you issued the invoice, the euro sat at one level; on the day you collected, it sat at another. The distance between those two points went somewhere. In your ledger it survives as a single line, and most of the time nobody looks at it a second time. It's a small number, and that is precisely the problem. Because it is small, it stays invisible. Because it recurs, it accumulates.

This article looks at why the FX difference — the gap that appears when a foreign-currency invoice is closed by a payment at a later date — is the quietest leak on a balance sheet, and why making it visible is a margin question for companies that import and export from Turkey. This is the exact spot where CFOs and accountants most often say "probably just an FX difference, let's move on." And it is exactly there that the cost piles up.

Three terms, one sentence each

This article turns on three technical terms, so let's define them at the door. Leaving the jargon outside lightens the mental load for everything that follows.

- CBRT official rate: The exchange rate the Central Bank of the Republic of Türkiye (CBRT) publishes each day. It is the reference figure you use to convert a foreign-currency transaction into lira. When two parties disagree over which rate applies in a reconciliation, both fall back to this official rate.

- FX difference: The gap that arises when a foreign-currency invoice is converted to lira not at the rate on its issue date but at the rate on the date it is paid or closed. In other words, the difference that time creates.

- Cross-currency closing: When the invoice currency and the payment currency differ — a EUR invoice settled by a TL payment, for example. The closing is the calculation of which rate that payment used to cover that invoice.

Put the three together and you get one of the balance sheet's quietest line items. We walked through how these terms interlock in our piece on reconciling foreign-currency invoices with the CBRT official rate; this article builds on that ground and adds the dimension of *accumulation*.

The difference isn't an error; it's the trace of time

Say the CBRT rate was 35 TL on the day you issued the EUR 10,000 invoice: 350,000 TL on the books. If the rate had moved to 36 TL by the time your customer paid two months later, the lira equivalent comes to 360,000 TL. The 10,000 TL gap between them is not a typo — it is the natural consequence of the rate moving between two dates. Accounting records it as either "FX gain" or "FX loss."

So far, everything is by the book. The issue is not that the difference *exists*; it's whether it is *visible and traceable*. Because 10,000 TL on one invoice becomes millions across hundreds of foreign-currency invoices. And in most companies that total is never gathered in one place or managed as a whole; it dissolves inside each individual closing.

An FX difference is not an error; it is the trace of time. The problem is not that it exists, but that it is scattered across hundreds of lines and never totaled anywhere.

Grasping this distinction is critical. Most of the gaps a company meets in foreign-currency reconciliation are genuinely legitimate — compliant, explainable, properly recorded FX differences. Trying to erase them as "errors" pulls your ledger away from reality. But the reverse is equally true: waving every gap through as "just an FX difference" buries a real inconsistency. Drawing the right line between these two extremes is what this article is really about.

"Is this an error, or an FX difference?"

That is the real question. The gap between a foreign-currency invoice and the payment that closes it can be one of two things:

- An FX difference: If the gap is *explainable* by the rate movement between the two dates and sits inside a reasonable band, it's normal — record it and move on.

- An inconsistency that needs review: If the gap cannot be explained by the rate movement over that window — if it falls outside the reasonable band — there may be a short collection, a mismatched payment, or a missed item behind it.

Made by hand, this distinction is punishing work. For every foreign-currency invoice you'd have to line up the issue date, the closing date, the CBRT rate on both days, and the actual amount collected. A person can do that for ten invoices. Nobody can do it for thousands — and because they can't, they default to "probably an FX difference" and move on. This is exactly where real debt and phantom debt blur into one another.

Who draws the reasonable band?

"Reasonable band" sounds abstract, but it is in fact a computable range. The movement between the CBRT rate on the invoice's issue date and the CBRT rate on the payment date sets the boundaries of what the difference *should* be. If the gap sits inside that boundary, the explanation is ready-made: time passed, the rate moved, and the invoice carries the trace of that move. If the gap sits outside it, something other than the rate is behind it.

We show how to systematize this assessment step by step in our article on reconciling EUR/USD invoices against the CBRT official rate. The logic there: for every cross-currency closing, compute the expected lira equivalent from the official rate, compare it against the amount actually collected, and place the deviation on a range. What lands inside the range is an FX difference; what lands outside is a signal.

Timing widens the gap

One point deserves underlining: the FX difference grows in direct proportion to how late an invoice is closed. On an invoice collected within a week, the gap is small; on one that stays open for six months, the rate has traveled a far longer road. Which means your collection discipline is, in fact, a form of FX risk management — most companies treat the two as separate headings, when they are two faces of the same coin.

That is why the age of your open foreign-currency receivables is not only a "who pays when" question. It is also a "which rate will my balance sheet realize when this receivable closes" question. Every late-closing foreign-currency invoice widens the pipe of the silent leak a little further.

Aging and FX risk on the same table

In periods when Turkish rate volatility runs high, this relationship sharpens. If your aging report shows a EUR receivable past 180 days, that line carries two risks at once: the risk of non-collection, and — even if collected — the risk that the rate converts the receivable into a lira value far from what you expected. The "age" of a foreign-currency receivable is, directly, the rate uncertainty under which it will eventually be realized.

For this reason, in foreign-currency reconciliation, collection tracking and FX-difference tracking cannot be separated. A company that keeps them in two different reports has split two halves of the same risk across two different desks — and nobody sees the sum.

The hidden tangle of cross-currency closing

There's one more layer that makes foreign-currency reconciliation hard: a payment rarely closes a single invoice, at a single rate, in a single stroke. In real life the pattern is far messier.

- A customer pays the total of three EUR invoices with one TL transfer. Which invoice closed at which rate?

- A partial payment arrives: the incoming amount ties to no invoice exactly, closing two in full and a third by half. Here FIFO — "first in, first out," the rule of closing from the oldest open invoice first — comes into play. But if each invoice was issued on a different date at a different rate, the closing order directly determines the size of the FX difference.

- The payment comes not from the customer itself but, on its behalf, from a group company or a collection agent — and in yet another currency.

In all three cases the gap forms not from a single rate movement but from several dates and several rates interlocking. We covered why partial payments and FIFO order make matching this hard in our piece on why payment-to-invoice matching is hard: FIFO and partial payments. Cross-currency adds a currency dimension on top of that tangle.

On a single foreign-currency invoice, the FX difference is one line. On a multi-payment, multi-date closing, it is a chain of calculations that depends on who was closed at which rate.

The gap can't be verified without three sources side by side

The only way to know whether an FX difference is genuinely an FX difference or an inconsistency is not to look at a single source. You have to bring at least three sources into the same line:

- The e-invoice: The invoice's currency amount, currency, and issue date — the source of the expected debt. ("E-invoice" here is the electronic invoice that carries the original obligation.)

- The bank statement: The lira (or foreign-currency) amount that actually landed and the collection date — the source of what actually happened.

- The ledger entry: At which rate and with what closing logic the invoice was booked — how the company itself interpreted the transaction.

Until these three meet on the same line, the question "where did the gap come from" cannot be answered. The invoice says EUR, the bank shows TL, the ledger applied some rate; you can only tell whether the gap arose from a rate movement or from something else by placing all three side by side. We opened up the logic of this three-source cross-check in full in our piece on bringing bank, e-invoice, and ledger together in three-way reconciliation; the FX difference is one of the places that three-way alignment earns its keep the most.

A check that looks at a single source is bound to go wrong here. Look only at the ledger and you assume the rate the ledger applied is correct — when that is precisely the thing that needs verifying. Look only at the bank and you can't know which invoice the incoming amount closed, at which rate.

Small line by line, meaningful in total

The insidious side of the FX difference is its scale. On a single invoice it's a few thousand lira — not a number to ruin anyone's morning. But in a company that lives on export or import, those "few thousand" repeat across hundreds of invoices. Summed, they produce an amount that appears in no report's headline yet bears directly on your true margin.

Consider it: a company issues hundreds of EUR and USD invoices across the year, each closing on a different date at a different rate. Each closing throws off a few thousand lira of FX difference — some in the gain direction, some in the loss direction. Looked at one by one, they're all "normal." But the net sum of these differences is the very line that sets that company's real foreign-currency margin. And in most companies that sum never appears anywhere as a single figure; it's scattered across hundreds of ledger entries.

That is exactly what "silent leak" means: every drop is small, but the pipe runs continuously and nobody is measuring the tap's total flow.

How iFinances makes the FX difference visible

iFinances doesn't recompute this layer; it makes it *visible*. It brings each foreign-currency invoice alongside the payment that closes it, the CBRT rates on both dates, and the amount actually collected. It surfaces whether the gap is explained by a reasonable rate movement. What's explainable stays an FX difference; what isn't gets flagged as a signal that a human eye should look at. The decision still belongs to the accountant — the system only shows which line to look at.

Concretely, the foreign-currency reconciliation view aligns the following for every cross-currency closing:

- The invoice's currency amount and the official rate on its issue date.

- The date the payment occurred and the official rate on that date.

- The gap between the expected lira equivalent and the actual amount collected.

- Whether that gap sits inside or outside the reasonable band explained by the rate movement between the two dates.

Items falling outside the reasonable band move to the anomaly detection layer: the system says "this gap can't be explained by the rate" and leaves the rest to a human. So real FX differences accumulate quietly while deviations the rate can't explain surface one by one. All of the product's reconciliation and matching modules work on the same principle: systematize the routine, leave the judgment to a person.

This is not about replacing the accountant. Quite the opposite: the hundreds of rate comparisons the machine computes systematically let the human turn their eye to the minority that genuinely requires judgment — the unexplained gap, the unusual closing, the missed item. The routine surfaces; what remains is the decision.

Frequently asked questions

Doesn't accounting already record FX differences? What does iFinances change?

Accounting records every FX difference faithfully — true. But those entries are scattered across hundreds of separate transactions; neither is their total visible in one place, nor has it been verified whether each one is "genuinely an FX difference or a hidden inconsistency." iFinances doesn't rewrite the entries; it places them alongside the e-invoice and bank statement and surfaces whether each gap is explained by the rate movement. So it makes visible not the entry, but the *accuracy and total* of the entry.

What happens when a gap falls outside the reasonable rate band?

The system flags that gap as a signal and brings it in front of the accountant — but it makes no decision itself. An unexplained gap can mean a short collection, a mismatched payment, a missed item, or an invoice booked at the wrong rate. Which of these it is becomes clear when a human looks behind the line. The job of iFinances is to put the right question on the right line in front of you; the judgment that answers it stays with you.

Does this only apply to exporters?

No. Any company that issues foreign-currency invoices or makes foreign-currency payments — exporter, importer, or a firm signing FX-denominated contracts domestically — is exposed to the same leak. An FX difference arises anywhere the invoice currency or the payment's currency or dates differ. As your count of foreign-currency items grows, you cross the threshold where manual tracking breaks and systematic verification starts to matter.

Turning the silent leak into sound

The FX difference is already inside your ledger. It was there in every foreign-currency closing. What was invisible was never the number itself — it was how much it added up to, which invoices it came from, and whether it held a real FX difference or something else. The silent leak only becomes audible once you gather the items and put them on the same screen.

If you'd like to see how much of this layer has accumulated in your foreign-currency reconciliation, get in touch with iFinances — let's measure the flow rate of the silent leak in your own data, together.

✦ iFinances — See what you're missing.

One post a month.

Get new insights straight to your inbox. No spam, just well-crafted reads.